To Roth or not to Roth? This is the question I get the most from people who are mid-career and in the thick of their wealth accumulation phase.

While each person’s specific answer is complicated and should be personalized to their unique situation, there are some universal principles to understand as you think about this. And also note that there actually IS no "right answer" to the Roth vs Traditional question. It depends on what you choose to believe about the future - we’ll get to that.

But for starters, let’s get the basics out of the way. Sometimes it’s helpful to understand WHY something exists and HOW it came about. This stuff can be dry, so maybe a story?

Part 1: Understanding the Origins

Employers to Employees in the 1980s: “It’s all you, bro.”

Back in the 1980’s employers switched from defined benefit plans (ie. pensions) to defined contribution plans (ie. 401ks) to fund employee retirement. The difference is: in a defined benefit plan the employer promises a certain outcome or benefit to employees and in a defined contribution plan, the onus is on the employee to manage their retirement outcomes. The rationale for the switch is obvious - pension plans weren’t delivering as expected and employers didn’t want the responsibility so they shifted to an approach that put individual employees in control.

In order to drive employees to this new model, one of the incentives was that employees could put dollars into their new retirement accounts without paying taxes (for now.) Any money contributed to a 401k would reduce your taxable income and thus lower your tax bill. The government would simply tax these retirement contributions and all the earnings when the funds were taken out during retirement.

It was actually a pretty smart move for the government to do it this way. In today’s dollars, you can invest $23,000 (the maximum you can contribute in 2024) and pay no tax! Congrats! You invest that in an index fund that grows on average 6% per year, let it simmer for 30 years and now you get to pay tax on the resulting $132k that you have in your account at retirement. It’s not hard to see how this is even a worse deal if you are younger - the lower your income (and resulting tax bracket) is today and the longer your money has time to grow, the worse this deal potentially gets.

They’re Politicians, Not Marketers (or Educators)

The shift away from pension plans was a MASSIVE change in strategy. And all of this happened during a time when information was a bit harder to come by, a time before Nerd Wallet, if you can even comprehend such a time.

Not surprisingly, the government isn’t so great at marketing. Or education. As you might imagine, adoption wasn’t quick. There’s an entire generation of middle-class Americans who didn’t embrace this as they should have and have entered retirement completely dependent on Social Security with low or no retirement account balances. Low retirement account balances mean low tax revenue being collected. And that means the government’s budget doesn’t work.

Compound that mess with the fact that when all of this change first happened, not all employers even offered 401ks, especially smaller employers. How is someone supposed to fund retirement if they don’t even have access to a retirement plan?

Enter: The Roth

One reason the Roth was introduced was to increase accessibility to tax-advantaged retirement savings but to do so in a way in which the government didn’t have to take a big revenue hit by delaying those tax payments. This new approach allowed for investment now, but you also pay the government the tax due now. And so Roth was born in 1998. More people with access means more taxes collected now to balance the budget. Right?

The problem was, the availability of the Roth was somewhat exclusive to begin with - you had to make under a certain amount of money. But wait - if you make under a certain amount of money, you - by definition - have less to invest, which means less tax to pay. That’s not going to solve any budget deficits.

Part 2: Government Budgeting & Fiscal Policy

About Government Budgeting

A quick but important word on government budgeting. Congressional budgets are done in 10 year cycles and no one involved seems to care much about what happens after the current 10 year cycle ends. Make it work today, and kick the can on everything else. This is an important facet of our story.

The Government’s Payday Loan because, YOLO.

Ok so it’s 2010. Government spending is out of control, national debt is through the roof, and Social Security is…not doing well. By now, defined contribution plans have picked up as the retirement savings vehicle of choice for Americans so there’s a bunch of tax money in the system in traditional vehicles like IRAs or 401ks, but the tax on many of those assets isn’t due for a loooong time. Longer than most Congressional folks will be in office.

What’s a short-sighted way to solve a long-term budget issue when you’re desperate? A payday loan, of course. Take less money now instead of more money later!

The government decided to lessen the regulations on Roth access to see if wealthy investors would convert their savings and pay the tax now instead of later. They were willing to take less money in order to have that money NOW. Because who cares what happens later? YOLO in Congress, amirite?

And so, as part of an extraordinarily short-sighted fiscal gimmick to help correct the massive budget deficit, you could convert an unlimited amount of money from traditional to Roth vehicles.

When regulations loosened up in 2010, wealthy investors did just what was expected, en masse. Roth conversions were up 9x in 2010. As of 2017, there’s $810 billion in Roth accounts - all of which will keep growing and never have a tax bill incurred.

Recent Expansions

More recently, Biden approved the SECURE Act 2.0 in 2022 which is the biggest boon Roths have seen to date. Employers can match in a Roth 401k. Self Employed folks can set up Roth SEP IRAs. Kids decide to forego college? Roll that 529 into - you guessed it - a Roth IRA. My husband has access to an automatic cash sweep Roth program in which we contribute post-tax dollars and before we can accrue any earnings on it, it’s automatically swept into a Roth, so we never owe a dime more in taxes - like MAGIC. It’s a cash grab by the government to try to get the budget to work.

So while your ability to directly contribute to a Roth is limited by your income and capped at $7,000, you can roll over quite literally as much as you want. $12 million in a traditional IRA? Pay tax on it now and never again by rolling it into a Roth.What a horrible decision for lawmakers to kick the can to their successors, and an incredible opportunity for investors to take advantage of years and years of tax free growth on their retirement balances.

Part 3: Strategic Considerations

A good strategy for improving growth in your retirement accounts is to minimize the impact of taxes. Taxes are inevitable, so if you think taxes are low right now, then you want to pay them now. If you think they’re high, you want to wait and pay later when they are lower. I am not here to predict where taxes are going, but I will give you 3 things to consider and you can take away from them whatever you like.

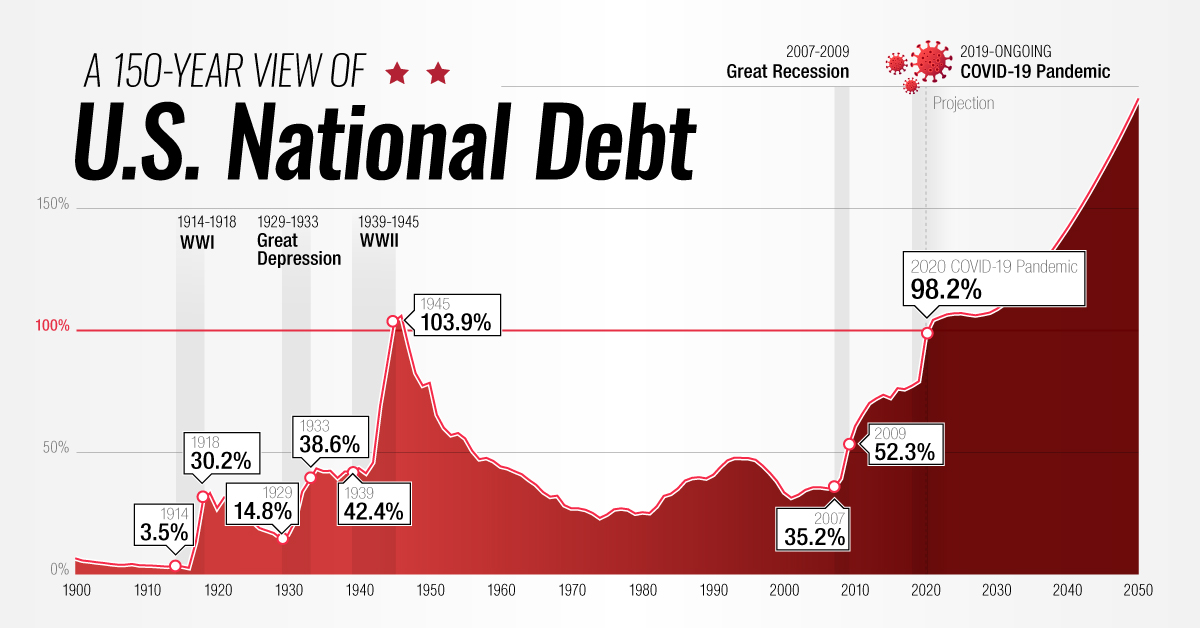

This is what the national debt looks like, including predictions for the future:

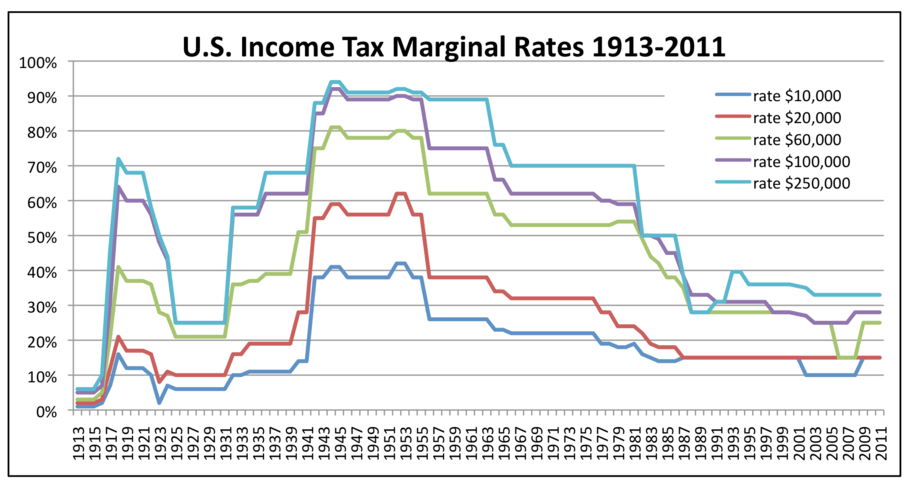

This is what tax rates have looked like historically:

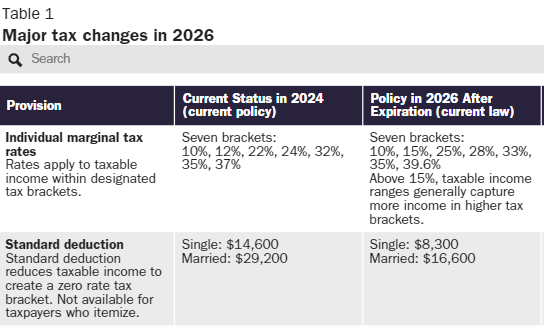

The table below outlines what is currently set to happen automatically to tax brackets and deductions in January 2026 when the Tax Cuts and Jobs Act expires.

Note that there’s an election between now and then, and whichever party wins has a point of view on what they’d like to do here (let taxes revert to the previous/higher levels, extend the TCJA discounted tax table, or something else entirely)

You can come to whatever conclusion you like about future tax rates based on this information, I'm no fortune teller.

Getting Sneaky Ideas

What If I just live off of Social Security or other assets and never draw from my retirement account? I can leave it to my heirs and I’ll never have to pay the tax! Not so fast. They thought of that. If you don’t take the money out of your traditional accounts by a certain age, you will actually be forced to do so via Required Minimum Distributions (RMDs) to ensure the government gets the taxes that are due. More on this later.

Making a Bet on the Future

So here’s the deal. You can pay all the tax now (at a known tax rate), let your money grow, and never pay tax on it again.

Or you can take a tax deduction now, let your money grow and pay tax (at a rate that you don’t know) in the future.

Here’s how to think about that: If you believe taxes (and your specific tax bracket) are going to go up from where they are now, then it makes sense to forego the tax deduction and pay at today’s reduced rates.

If you think taxes (and your specific tax bracket) are going to go down from where they are now, then take the tax deduction and pay taxes later.

You want to have taxable income when taxes are low, and tax deductions when taxes are high. And you are making a bet on your hypothesis by choosing Traditional vs Roth.

Some More Considerations

A few more things to consider:

Won't my tax bracket be lower in retirement?

People sometimes think that their tax bracket will certainly be lower in retirement - after all, you aren’t working. However, if you ask most tax planners or accountants they’ll tell you that for a lot of people once you hit the top tax brackets, you end up staying there. You have made enough money that you have likely saved a lot of money, and that tax bill is all going to come due via Required Minimum Distributions in retirement. Plus you have no childcare deductions, no 401k deductions and maybe not even a mortgage deduction in retirement. It’s entirely possible that you end up making more in retirement that you do during your working years if you’ve been a good saver.

What’s the downside of doing Roth and paying tax now?

Assuming you have time to let your money grow, the worst case scenario here is that you pay your tax on a Roth contribution or conversion and now you’re locked into a zero percent tax rate for your entire life (and ten years beyond that for your heirs.)

Speaking of heirs, is there a chance you’re leaving money behind as an inheritance?

If so, there’s a high likelihood that you’re leaving it to someone who is midlife and at the peak of their earnings. You can pay it for them by converting, and they’ll owe nothing and the value isn’t even considered part of your estate in terms of taxation.

Roth FAQs: The Boring Stuff

What’s the main difference between Roth IRA (or 401k) and Traditional IRA (or 401k) Accounts?

The key difference is in how the accounts are taxed. If you contribute to a Roth, you are paying taxes now, at your ordinary income tax rate. You can find those tax tables for 2024 here. Once you pay this tax, your money grows and you aren’t taxed on it again.

With a Traditional Account, you’re electing to defer your tax payment until you take the money out, which ideally wouldn’t be until you retire. All the money you have contributed and any growth that has accumulated over the years will all be taxable at your ordinary income tax rate when you take money out. You can see how if your money is given a lot of time to grow, you could end up with a pretty hefty tax bill when you start to use this money.

How do I access a Roth?

In order to contribute directly to a Roth, outside of an employer sponsored plan, you have to make under a certain amount annually. You can find those amounts here.

If you make more than the threshold to open a Roth IRA, don’t worry - over the past few years MANY more employers have started offering Roth 401k options and there’s no income limit on those. (Though you can only contribute up to the maximum 401k annual contribution limit which is $23,000 in 2024.)

The last option is to convert some of your traditional retirement savings into Roth. You’ll need to have cash on hand in order to pay the tax, but there is zero limit on how much you can convert and there’s no income limitations.

When is the best time to convert?

The best time to convert is the end of the year. By this point you’ll know what your income was for the year and can calculate what the tax would be on a conversion. You’ll need to have cash to cover the tax bill so that also factors into your timing and the amount you can convert.

If you have a lot to convert, you can do it over the course of a few years. But remember, tax brackets are going to do *something* in January 2026 at which point your rate might change.

When can I access the money?

In a Roth, you can actually access any of your contributions at any time. This is your money, that you paid taxes on, and you can get it back at any time for any reason. Some people love the flexibility that gives them.

In order to access the earnings in your Roth account you need to meet a few criteria. If you are 59.5 or older and have had a Roth account for at least 5 years, there’s no penalty and you’re free to do what you want with the contributions AND the earnings. If you are younger than that or haven’t had your account for 5 years, there are still a few loopholes that let you access your full balance (contributions + earnings) -

- College expense for you or a dependent

- Down payment on a primary residence

- Unreimbursed medical expenses

- To prevent eviction or foreclosure

More details on those exceptions can be found here.

If you don't meet any of the above criteria and you pull out earnings from your Roth, you'll incur a 10% penalty.

What else should I know?

One big thing to know is that with a Traditional (i.e. Pre-tax) account, you are forced to take Required Minimum Distributions (RMDs) starting at age 73. This is basically the government coming for what you owe them in taxes - you can’t hold on to it any longer. Based on your age and life expectancy you have to withdraw and pay tax on a portion of your traditional retirement account balances.

With a Roth, you’ve already paid tax so the government doesn't force you to do anything with your balance as you age. This gives you a lot of flexibility in tax planning and can be much more advantageous for your heirs should you leave any money behind at your death. You’d be leaving them contributions and earnings that have a tax bill that is paid-in-full which is really ideal.

Why do RMDs matter?

Depending on your age, it may seem like RMDs are such a distant thing to worry about. But that’s exactly the problem - if you’re young, your money has a LONG time to grow. The big unknown X factor in all of this is tax rates. As of today (March 2024) we’re still benefiting from the Tax Cuts and Jobs Act of 2017, which lowered tax rates for most Americans. This tax table expires on January 1, 2026 and reverts to the prior tax table, which is going to be unfavorable for most. Add to that the growing amount of debt the government is dealing with, and it’s hard to see a future where taxes get any cheaper than they are today. If you believe we’re at a low point right now, it’s like taxes are on sale through the end of 2025, and you have a chance to pay them now before they get hiked back up to prior levels (and possibly even higher)

What about Traditional IRAs?

I don’t actually understand why you would put money in a Traditional IRA right now. If you’ve already maxed out your 401k contribution and are looking for the next logical thing to invest in, the only possible benefit you’d get from a Traditional IRA contribution is a tax deduction, assuming you aren’t phased out based on income. You’d be putting your money in a vehicle that has all kinds of restrictions on when and how you can get the money, along with a growing tax bill. Instead, why not just put extra funding in a brokerage account? You’ll pay capital gains tax on your earnings (which is lower than income tax rates) and you can get to your money whenever you want it, or save it up for retirement.

In Conclusion

Look, the government LOVES Roth right now.

Regulations are loosening and more people than ever have access to contribute to a Roth.

Why? The government needs cash.

So you’re basically giving them a payment now (which is likely at a discount) that completely fulfills your commitment to them, because well, they’re a little desperate.

For a very long time they pushed everyone into traditional accounts and conditioned us to think this is the very first and most basic thing we should invest in. But they have to wait a LONG time to reap those benefits (remember, you can delay paying taxes all the way to age 72!), so the Roth option becomes more appealing NOW.

In short, if any of the following sound like you, you may be better off with a Roth:

- Your money is going to have a significant time to grow.

- You believe your taxes will go up in the future.

- You may be leaving money behind as in inheritance.

- You value flexibility and access to your money.

- You would rather do a sure thing now vs wait and see what the future will hold.